If you run a nonprofit, funders, boards, auditors, and the IRS all expect one thing: clear, defensible answers to the question “How did you spend the money?” The statement of functional expenses allocation is the document that answers that question. It translates every dollar your organization spends into the functions it supports — program services, management and general, and fundraising — and shows stakeholders how resources further your mission. Get this right, and you build trust. Get it wrong, and you risk confusion, lost grant recoveries, or unpleasant audit findings.

Here’s the short version: the statement is a matrix that lists natural expense categories (salaries, rent, supplies) down the rows and assigns each expense, wholly or partially, to functional columns. The heavy lifting behind that neat table is your expense allocation method and the cost allocation plan that documents how you divided shared costs. This article walks through what the statement is, the methods you can use to allocate expenses, how the data maps to Form 990 Part IX, and how to write a cost allocation plan that holds up to auditors and funders. Ready? Let’s make your allocation approach simple, defensible, and useful.

Understanding the Statement of Functional Expenses

Definition and purpose of the statement

- What it is: a financial statement showing the organization’s expenses organized by natural classification (what was purchased) and functional classification (why it was purchased: program, management & general, or fundraising).

- Why it matters: donors and regulators use it to evaluate program efficiency and stewardship; auditors use it to test consistency and appropriateness of allocations; management uses it to budget, set indirect rates, and make resource decisions.

Functional categories explained

- Program Services: Expenses directly tied to delivering your mission (program staff salaries, program supplies, client assistance).

- Management and General (M&G): Administrative costs that support overall operations (executive salaries, accounting, legal, general office).

- Fundraising: Costs to solicit donations (development staff, events, fundraising communications).

Natural expense categories typically included

- Salaries and wages

- Employee benefits

- Professional fees (audit, legal, consulting)

- Rent and utilities

- Supplies and equipment

- Travel and conferences

- Grants and program assistance

- Advertising and fundraising costs

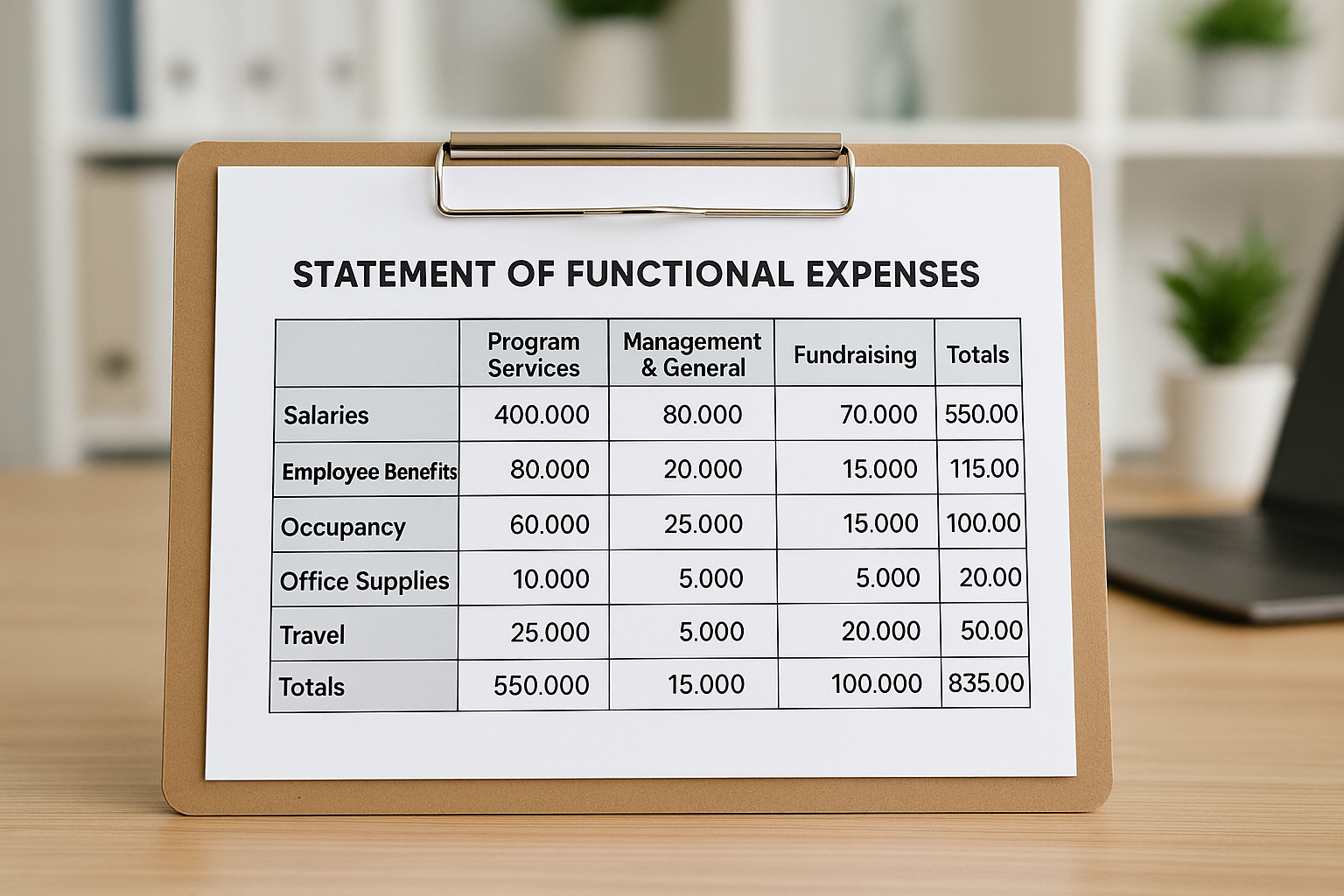

Presentation format (matrix/table style)

- The common format is a matrix with natural expenses as rows and functional categories as columns. Each row shows how a natural expense is allocated across functions, with a total at the end.

- This same matrix feeds Part IX of IRS Form 990, so consistency between financial statements and Form 990 is critical.

Quick example (simplified)

| Natural Expense | Program Services | Management & General | Fundraising | Total |

|---|---|---|---|---|

| Salaries | 120,000 | 30,000 | 20,000 | 170,000 |

| Rent | 36,000 | 12,000 | 2,000 | 50,000 |

| Supplies | 15,000 | 2,000 | 1,000 | 18,000 |

| Total | 171,000 | 44,000 | 23,000 | 238,000 |

Bottom line: the matrix is simple to read but only as reliable as the allocation rules behind it.

Nonprofit Expense Allocation Methods Explained

Direct allocation of expenses (when it’s possible, do it)

- Definition: Assigning the full cost of an expense to the single function that benefited (e.g., a program-specific trainer’s fee goes straight to Program Services).

- Benefit: Clean, defensible, easy to document.

- Practical tip: Policies should require staff to code expenses to the most specific program or function possible at the point of entry (expense report, purchase order).

Indirect/shared cost allocation (when costs benefit multiple functions)

- Definition: Distributing costs that support more than one function (rent, utilities, shared staff time).

- Key principle: Use an allocation base tied to a logical cost driver (square footage for rent, FTE or payroll dollars for HR support, time and effort for multi-program staff).

Common allocation methods and when to use them

- Simplified allocation (single driver)

- Use when your organization is small and a single reasonable driver (like FTE or total payroll) can accurately divide multiple shared costs.

- Pros: Simple, low administrative burden. Cons: Less precise for complex operations.

- Multiple allocation bases

- Different cost pools use different drivers (rent by square footage, IT by number of users, HR by payroll).

- Pros: More accurate; aligns cost drivers to expenses. Cons: Requires more tracking and documentation.

- Step-down (sequential) method

- Indirect cost pools are allocated in sequence, where service departments allocate costs to other service departments and final program/fundraising/admin. Often used in government accounting.

- Pros: Greater precision when inter-service relationships exist. Cons: Complex and usually unnecessary for smaller nonprofits.

- Activity-based costing (ABC)

- Identifies activities (grant reporting, client intake) and traces costs to activities, then to programs based on activity consumption.

- Pros: Highly accurate for large, diversified organizations. Cons: Resource-intensive to implement.

Choosing the right method for your nonprofit’s size and funding

- Small nonprofits: Direct allocation + simplified allocation base (FTE or payroll) usually suffices.

- Mid-size: Multiple allocation bases give better accuracy without extreme complexity.

- Large/complex nonprofits with many funding streams: Consider step-down or ABC, especially if federal grants require detailed indirect cost allocation or you negotiate a NICRA.

Typical allocation bases and drivers

- Time and effort (timesheets, activity logs) — best for salaries and payroll-related costs.

- Square footage — best for occupancy costs.

- FTE or headcount — useful for HR or benefits.

- Payroll dollars — good when cost relates to compensation levels.

- Participants or service units — useful when programs vary by output volume.

A simple salary allocation example

- Total payroll cost to allocate: $200,000.

- Program A staff FTEs = 6; Program B = 2; Admin = 2; Fundraising = 1. Total FTE = 11.

- Program A share = 6/11 = 54.5% → $109,091; Program B = 18.2% → $36,364; Admin = 18.2% → $36,364; Fundraising = 9.1% → $18,182.

- Notes: Always document FTE counts and the date they were calculated.

Functional Expense Reporting for Form 990 Part IX

Overview of Form 990 and its role

- Form 990 is the IRS information return many tax-exempt organizations file annually. It’s public and closely scrutinized by donors and funders.

- Part IX is the Statement of Functional Expenses — the IRS wants the same functional classification you use in your financial statements.

What Part IX requires

- A set of standardized natural expense rows (e.g., salaries, grants, occupancy) and functional columns (program services, management and general, fundraising).

- Filers must report totals that reconcile to the amounts on the financial statements and other parts of the Form 990.

Who must complete it and filing thresholds

- Most organizations required to file Form 990 must complete Part IX. Smaller organizations that file Form 990-EZ or Form 990-N have different requirements — check current IRS filing thresholds and instructions for your tax year.

Allocation requirements and IRS expectations

- Reasonableness: Allocations must be logical and supported by the organization’s practices.

- Consistency: Use the same methods from year to year unless you document and justify a change.

- Documentation: Maintain policies, timesheets, allocation calculations, and the cost allocation plan to substantiate entries.

Common pitfalls and compliance tips

- Mistake: Using inconsistent allocation methods across similar expense types or years without explanation.

- Mistake: Failing to document timesheets or cost drivers used for allocations.

- Tip: Reconcile the statement of functional expenses to Form 990 Part IX before filing. Have your finance committee review and sign off on methods annually.

- Auditors will test reasonableness and completeness; be ready with evidence.

Developing a Cost Allocation Plan for Nonprofits

What is a cost allocation plan (CAP)?

- A CAP is a written policy that explains how your nonprofit allocates indirect/shared costs across programs, fundraising, and administration. It’s the governance backbone for your functional expense statement and Form 990 disclosures.

Why nonprofits need a CAP

- Compliance with federal grants (2 CFR Part 200 Uniform Guidance) often requires a documented method for allocating indirect costs.

- Supports consistent budgeting, grant billing, and rate setting.

- Demonstrates stewardship to donors and the board.

Essential elements of a CAP

- Scope and purpose: Which funds and costs the plan covers.

- Definitions: Direct costs, indirect costs, cost pools, allocation bases.

- Cost pools: Groupings of related indirect costs (occupancy, administrative services, IT).

- Allocation bases and drivers: Justification for each base chosen.

- Methodology: Step-by-step description of how each cost pool is allocated.

- Documentation requirements: Timesheets, FTE counts, space plans, invoices.

- Review process: Who reviews the CAP and how often it will be updated (typically annually).

- Approval: Board or finance committee approval signature and date.

Step-by-step process for creating and implementing a CAP

- Inventory your expenses by natural category for a recent fiscal year.

- Identify direct costs and ensure they’re coded to programs at source.

- Group remaining shared costs into logical cost pools.

- Choose allocation bases tied to cost drivers for each pool.

- Calculate allocations using an agreed methodology and produce a draft statement of functional expenses.

- Document assumptions, data sources, and calculations.

- Present the CAP and statement to the finance committee or board for approval.

- Implement in accounting systems (expense codes, classes, projects).

- Monitor and update annually or when programs/facilities change.

Best practices and regulatory standards

- Keep it simple enough to be consistently applied but precise enough to be defensible.

- Use time and effort certifications for significant multi-function payroll allocations.

- Retain supporting records for at least the period required by grants and state law (often three to seven years).

- If you negotiate an indirect cost rate with a federal agency (NICRA), align your CAP with the rate agreement.

Sample cost allocation policy language (short)

“Our organization allocates indirect costs to programs, management and general, and fundraising using cost pools with identified allocation bases. Payroll-related indirect costs are allocated on an FTE basis. Occupancy costs are allocated by square footage. Time and effort reports are used to allocate multi-program staff salaries. The Chief Financial Officer will review allocation results annually and present recommended changes to the finance committee.”

Checklist for Form 990 Part IX preparation

- Reconcile total expenses on financial statements to Form 990.

- Verify each natural expense row maps to your chart of accounts.

- Confirm allocation methods are documented and approved.

- Retain supporting calculations and drivers for at least the filing year.

- Have a second-party review (ED, CFO, or board finance chair) before finalizing.

- Flag any material changes in allocation methods in your notes to financial statements.

Audit readiness tips

- Prepare a one-page summary of allocation methodology for auditors.

- Keep time and effort records accessible for payroll allocations.

- Be ready to demonstrate why your chosen allocation base reasonably reflects the benefits received.

- If an auditor requests more precise allocation, show how you plan to improve the methodology and document the limitations.

When to consult a professional

- You should consult a CPA or grant compliance specialist if:

- You manage significant federal grants and need a NICRA.

- Your allocation methodology is under question by a funder or auditor.

- You lack internal capacity to design a defensible CAP.

- Quick plug: Telos CPAs works exclusively with nonprofits and can help draft CAPs, reconcile statements for Form 990, and prepare audit-ready documentation if you need expert support.

Final checklist and next steps

- Review your current statement of functional expenses and confirm allocations are documented.

- If you don’t have a written cost allocation plan, draft the essential elements and get board or finance committee approval.

- Institute periodic reviews (annual is usually fine) and update your plan whenever staffing, space, or program mix changes materially.

- Train program and finance staff on coding expenses correctly at the source — it reduces allocation rework later.

A brief legal/accounting disclaimer

This article provides general information about nonprofit accounting and compliance. It’s not a substitute for professional advice tailored to your organization’s facts and circumstances. Consult a CPA or attorney for specific questions about taxes, audits, or federal grant compliance.

Wrap up

The statement of functional expenses is more than a filing requirement — it’s a transparency tool that clarifies how your organization uses its resources. A clear, documented cost allocation plan and reasonable allocation methods make that tool reliable and defensible. Start by insisting on direct allocation where possible, group shared costs into logical pools, pick allocation drivers that reflect real cost behavior, and keep the plan current and documented. Do that, and you’ll make life easier for your board, your auditors, and the people who fund your mission.

Want help turning your numbers into a defensible statement and a board-ready cost allocation plan? Reach out to a nonprofit-focused CPA — they’ll save you time and headaches and help you tell the financial story your donors expect.