If you run a small or mid sized nonprofit, congratulations — you’re tasked with changing the world while juggling spreadsheets, grants, and a board that thinks “cash flow” is a new yoga pose. Let’s be real… nonprofit accounting isn’t just bookkeeping dressed up in nicer fonts. It’s a stewardship system that proves you used donors’ money the way you promised, keeps you audit ready, and helps your board make smart decisions.

This guide pulls together the essentials: fund accounting for nonprofits, ASC 958 revenue recognition, nonprofit payroll compliance, and a tight month‑end close that doesn’t make you cry. It’s practical, example‑rich, and written so your exhausted ED at 11pm can actually use it. Hot take incoming: good bookkeeping is mission critical. Let’s dive in.

1 Understanding Nonprofit Accounting and Bookkeeping Basics

Nonprofit vs for‑profit — the headline: you measure success differently. For‑profits track owners’ equity; nonprofits track net assets. The mission is the bottom line.

Key differences and basics

- Mission focus over profit. Financials show sustainability and stewardship, not owner returns.

- Net assets not equity. GAAP requires classifying net assets as with donor restrictions or without donor restrictions.

- Fund accounting for accountability. You segregate funds to respect donor intents.

- Governing standards. FASB ASC 958 governs contributions and net asset classification; ASC 606 covers exchange transactions like fee-for-service.

- Bookkeeping is the day‑to‑day engine. Record donations, grants, expenses, reconcile bank accounts, and produce reports that answer: did we spend this grant correctly?

- Internal controls matter. Segregate duties, require approvals, keep digital trails, and retain documentation per grant and IRS rules.

Wrap up: Strong bookkeeping equals stronger stewardship — which equals trust from donors and fewer surprises. Nice.

2 Setting Up Fund Accounting for Your Nonprofit

What is fund accounting and why it matters Fund accounting is an accountability system. Instead of hiding donor restrictions in a memo, you give each purpose its own lane: general operations, program A, grant X, capital campaign. That makes reporting and compliance practical, not theoretical.

Key fund types

- Unrestricted (net assets without donor restrictions): board can use at will.

- Temporarily restricted (net assets with donor restrictions): use limited by purpose or time.

- Permanently restricted (endowment): donor requires principal remain intact.

Structuring a chart of accounts

- Start with natural accounts (cash, revenue, salaries) and add fund identifiers.

- Use segments: e.g., Account Number | Fund Code | Program Code | Class.

- Example scheme: 1000 Assets, 2000 Liabilities, 3000 Net Assets, 4000 Revenue, 5000 Expenses — then add Fund 01 = General, Fund 02 = Youth Program, Fund 03 = Grant XYZ.

Implementing in software

- QuickBooks Online Nonprofit: use Classes for programs and Locations for funds.

- Aplos: built for fund accounting with built‑in fund and donation tracking.

- Blackbaud, Sage Intacct, MIP: enterprise options with robust fund/subledger features.

- Tip: configure software so every donation entry includes donor, fund, restriction, and campaign fields.

Practical example of fund entries

- Unrestricted donation (cash gift to general operating fund)

- Dr Cash (Fund 01) $5,000

- Cr Contribution Revenue — Without Donor Restrictions $5,000

- Temporarily restricted grant for program supplies (grant award received)

- Dr Cash (Fund 03) $10,000

- Cr Contributions — With Donor Restrictions (Program Supplies) $10,000

- Spending restricted funds on supplies

- Dr Expense — Program Supplies $7,000

- Cr Cash $7,000

- When restriction is satisfied:

- Dr Net Assets With Donor Restrictions $7,000

- Cr Net Assets Released from Restrictions $7,000

Wrap up: Fund accounting is just disciplined bookkeeping with a purpose — and your future audit file will thank you.

3 Navigating ASC 958 Revenue Recognition for Contributions

Okay, so ASC 958. Sounds scary. It’s actually a decision tree that keeps you from recognizing revenue too early.

Decide whether it’s a contribution or an exchange

- Contribution (ASC 958): donor doesn’t get commensurate value back. Think general gifts, grants with no direct goods or services.

- Exchange transaction (ASC 606): donor pays for goods/services with commensurate value — event fees, memberships that include value.

Conditional vs unconditional contributions (the big distinction)

- Unconditional contributions: recognize revenue when promised or received (pledges recorded when promised; discount to PV if multi‑year).

- Conditional contributions: have BOTH a barrier to overcome and either a right of return or release. Money received before a condition is met is a liability (refundable advance) until the condition is satisfied or waived.

Donor restrictions vs conditions — don’t confuse them

- Restriction = class of net assets (with donor restrictions). You can recognize revenue for unconditional restricted gifts immediately; you just report them in the “with donor restrictions” class and release as restriction is met.

- Condition = revenue deferred until the condition is met.

Gifts‑in‑kind and agency transactions

- In‑kind assets: record at fair value, disclose usage and valuation method.

- Agency transactions: if you’re just passing funds through (you don’t have control), record a liability, not revenue.

Quick ASC 958 decision steps (no flowchart, but easy)

- Is there commensurate value to the donor? Yes → ASC 606. No → ASC 958.

- Is the transfer conditional (barrier + right of return/release)? Yes → Record liability until met. No → Recognize contribution.

- Does donor impose restrictions? Yes → Classify net assets with donor restrictions. Track and release when met.

Practical tip: review grant agreements line by line. If a funder says “we’ll pay when you reach X” — that’s likely a condition, not a restriction.

Wrap up: ASC 958 keeps recognition honest — don’t rush to call a grant revenue until the conditions are actually met.

4 Ensuring Payroll Compliance in Nonprofits

Payroll isn’t more fun here than anywhere else, but there are nonprofit quirks you must know.

Payroll tax basics

- Nonprofits still withhold federal income taxes, Social Security and Medicare (FICA), and generally match FICA — just like any employer.

- Many 501c3s are exempt from FUTA (Federal Unemployment Tax) but must check IRS rules and state unemployment obligations.

- File Forms 941 or 944 for federal employment taxes; W‑2 for employees.

Worker classification

- Employees vs independent contractors vs volunteers — misclassification is expensive. Use IRS tests and treat compensation accordingly.

- Volunteers typically aren’t subject to payroll taxes but document their volunteer status and avoid treating them like employees.

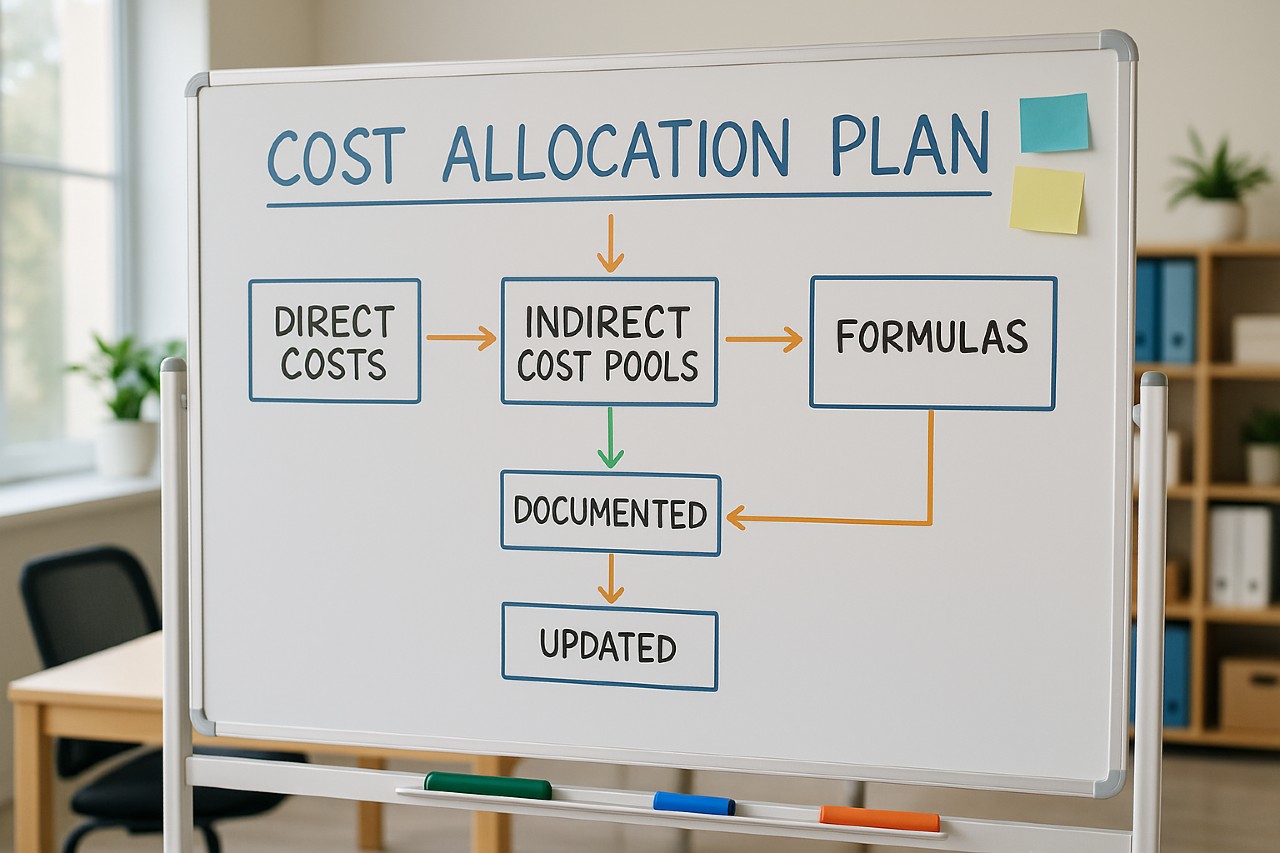

Functional expense allocation

- Grants and some funders require payroll to be allocated across program, admin, and fundraising.

- Use timesheets or effort reports. Example allocation entry:

- If Employee A works 70% program, 20% admin, 10% fundraising:

- Record gross payroll in payroll clearing or by employee, then allocate portions to respective functional expense accounts when posting.

Payroll documentation checklist (copyable template)

- Up to date Form W‑4 for each employee

- Job descriptions and signed offer letters

- Time and attendance records or effort reports

- Payroll register and paystubs

- Quarterly Form 941 and annual W‑2s filed

- State withholding and unemployment filings

- Proof of FUTA exemption eligibility if applicable

- Compensation policy approved by board for key staff

System recommendations

- Use payroll providers that allow project or class tracking: Gusto, Paychex, ADP (with cost center tracking), or integrated nonprofit payroll in Blackbaud/QuickBooks Nonprofit.

- Ensure payroll system exports to your accounting software for easy posting.

Wrap up: Payroll compliance = fewer headaches, less risk, and clearer program cost reporting. Sounds worth an afternoon.

5 Conducting an Effective Nonprofit Month End Close

Month‑end close is your monthly financial health check. Do it right and your board will stop asking for “ballpark” numbers.

Purpose and timeline

- Objective: accurate monthly financials showing activity by fund, program, and function.

- Best practice target: close and distribute financial statements by the 10th–15th of the following month. It’s a best practice, not a rule, but it keeps everyone informed.

Pre‑close checklist (copyable template)

- Collect donation and grant receipts; record all bank deposits.

- Reconcile bank and credit card statements.

- Confirm payroll entries and accrued payroll liabilities.

- Record accounts payable and matched expenses.

- Review grant budgets and restrictions; update grant schedules.

- Post depreciation, amortization, and accrual journal entries.

- Allocate shared costs (rent, utilities, admin) across functions.

- Review outstanding conditional contributions and refundable advances.

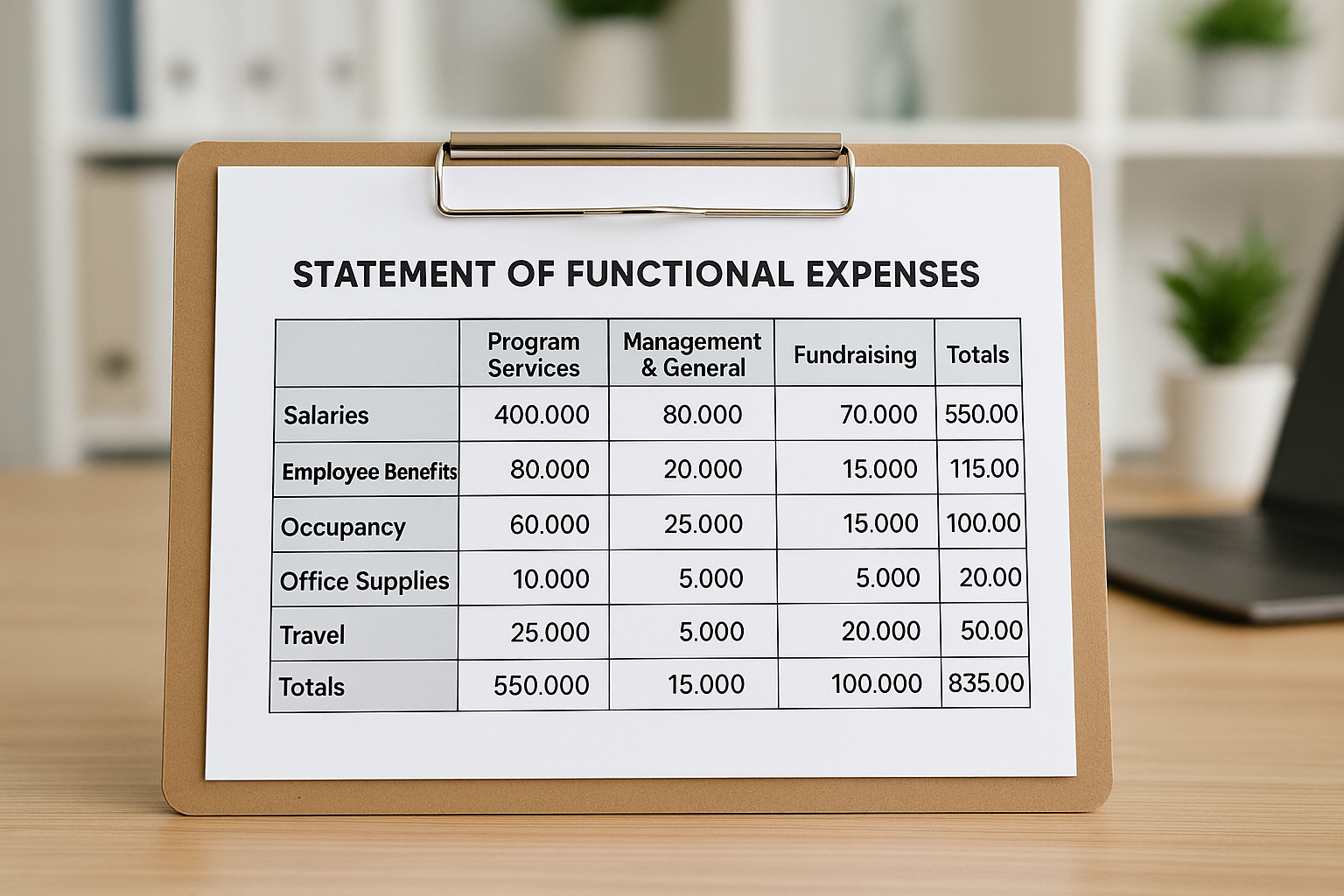

- Produce Statement of Financial Position, Statement of Activities, and Statement of Functional Expenses.

- Prepare a budget vs actual report with explanations for significant variances.

Sample journal entries for common month‑end events

- Accrued payroll (if pay date falls next month)

- Dr Salaries Expense $12,000

- Cr Accrued Payroll Liability $12,000

- Depreciation

- Dr Depreciation Expense $500

- Cr Accumulated Depreciation $500

- Allocate shared admin rent across programs

- Dr Program Expense — Rent $1,000

- Dr Admin Expense — Rent $200

- Cr Rent Payable $1,200

Communicating results

- Provide a one‑page dashboard for the board: cash on hand, burn rate, restricted balances, YTD variances, and top risks.

- Attach grant compliance notes and any fund restriction movements.

Wrap up: A disciplined month‑end gives you timely insight, credible reporting, and fewer surprises at board meetings. Win.

Software and configuration tips to close the loop

Recommendations

- Small orgs: QuickBooks Online Nonprofit or Aplos for easy fund tracking.

- Growing orgs: Sage Intacct Nonprofit, Blackbaud, or MIP for multi‑entity/fund complexity.

- Payroll: Gusto, ADP, or provider that supports classes/cost centers.

Configuration tips

- Use Classes or Locations to track programs and funds.

- Build fund-based subaccounts for grants requiring separate tracking.

- Map software reports to your nonprofit financial statements (statement of activities, position, functional expenses).

- Automate recurring entries: payroll allocations, depreciation, rent splits.

Wrap up: Pick tools that support fund accounting and make your month‑end a matter of routine, not heroics.

Conclusion

Here’s the thing… nonprofit accounting and bookkeeping are not optional bookkeeping chores; they’re the foundation of trust with donors, the backbone of grant compliance, and the roadmap your board needs to steward the mission. Adopt fund accounting, apply ASC 958 thoughtfully, keep payroll compliant, and close the month on a disciplined schedule. Get that right and you’ll be measuring impact, not just transactions.

If you want help setting up or reviewing systems, consider a firm that specializes in nonprofit accounting — Telos CPAs, for example, focus exclusively on nonprofits and can help tailor systems that scale with your mission.

Still reading? You’re my favorite. If you want, reply and I’ll send a downloadable month‑end checklist and payroll compliance spreadsheet you can copy into your accounting system. Buckle up — your next audit will be a breeze.