Introduction — Yes, grant accounting matters (and no, you can’t just “make it work”)

Ever get your hands on a grant award letter and think, “Is this legal mumbo jumbo secretly a treasure map?”

Welcome to the club. For nonprofit leaders, nailing grant accounting is not just about keeping the

books neat—it’s the thin line between making your mission happen and breaking out in a sweat explaining why

restricted funds bought pizza (true story).

So, buckle up. This guide is your no-fluff companion for real folks: founders, executive directors, board members,

and finance pros who want to actually understand what to track, when revenue shows up, how to honor those pesky

donor restrictions, and handle the ironclad demands of federal grants without losing

your mind. Expect stuff you can actually use today—yes, examples and checklists—and a no-nonsense peek at software

that won’t turn your ledger into a horror flick.

- Decode grant types without an accounting degree.

- Know when to say “revenue” vs “liability.”

- Stop mixing restricted funds with pizza money.

- Get audit-ready without losing your sanity.

Treat every grant like it’s funding your mission and auditioning you for your next one.

Understanding Nonprofit Grant Accounting Basics

What Is Grant Accounting?

Okay, here’s the thing. Grant accounting isn’t your everyday bookkeeping. It’s the special sauce of

tracking grant dollars so you don’t accidentally spend donor money on, say, that pizza slice we talked about. It’s

all about keeping funds apart, watching restrictions like hawks, figuring out who pays for what, and making sure

your paperwork would impress even the most hardcore auditor.

Why should you care? Because screw this up and you risk losing your funding, your rep, and face auditors squinting

at your books wondering what’s up with the “questionable expenses” line.

Track every grant dollar so clearly that your auditor could follow the story with a cup of coffee and zero drama.

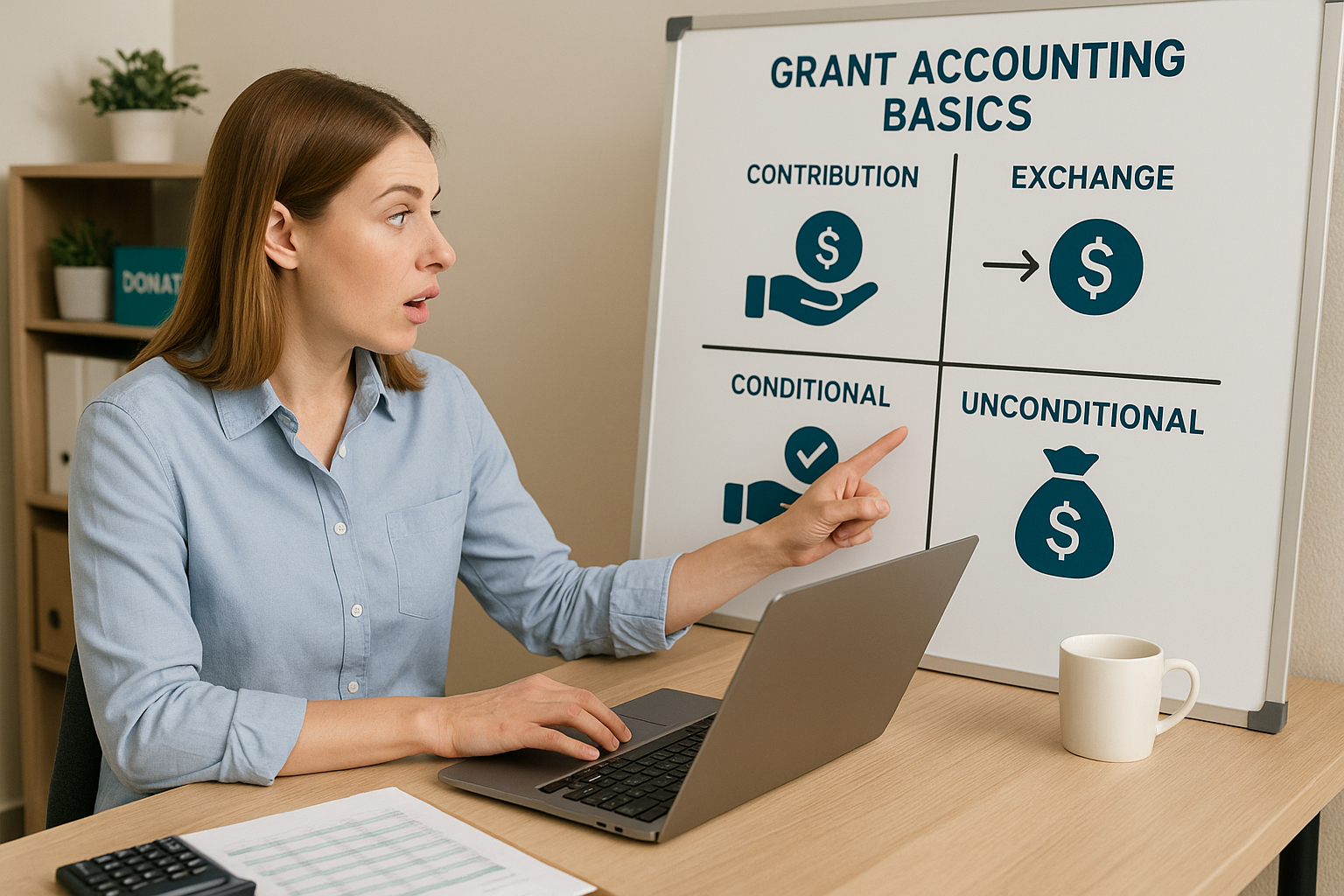

Types of Grants: Contributions vs Exchange Transactions

Hot take incoming: grants come in two flavors under nonprofit rules (thanks FASB ASC 958):

-

Contributions — basically, donors giving money with zero strings attached in return. You record

these as contribution revenue, but with a close eye on restrictions. -

Exchange transactions — here, you deliver goods or services back to the funder. These follow

contract revenue rules and change how you record and report.

This classification isn’t just semantics. It’s the key to when cash hits your books—and what the financial

statements say about you.

| Contribution | Exchange Transaction |

|---|---|

| Donor doesn’t get equal value back. | Funder receives goods/services in return. |

| Recorded as contribution revenue. | Follows contract/earned revenue rules. |

| Focus on restrictions (purpose/time). | Focus on performance obligations. |

Conditional vs Unconditional Grants

Cue dramatic pause… because this one’s important:

If your grant says, “Jump through these hoops or no money for you,” that’s a conditional grant.

You only count the cash as revenue once you’ve met the conditions (like delivering deliverables or hitting

performance targets). Until then, hold that cash with care—it’s a liability, not income.

On the flip side, an unconditional grant means the money is yours upfront. But if there are

donor-imposed limits (like “use it for this program” or “spend it by this date”), you recognize the revenue

immediately, then report it as net assets with donor restrictions until you fulfill the promise.

So yeah—figuring out if your grant is contribution or exchange, conditional or unconditional, changes when you say

“Cha-ching!” in your ledger—and whether you carry a refund liability on your balance sheet.

- “Do X or you don’t keep the money.”

- Recorded as a liability until conditions are met.

- Revenue recognized as milestones are achieved.

- Money is yours, but may have restrictions.

- Recognize revenue immediately.

- Track as net assets with donor restrictions until used.

Accounting for Grants in Not-for-Profit Organizations

Recognizing Grant Revenue Properly

Here’s what I’ve seen tripping people up:

-

Unconditional contributions? Count ’em as revenue the minute you get ‘em, but split between

restricted or unrestricted based on what the donor says. -

Conditional grants? Think of the money as “pending” until you knock out those milestones.

Recognize revenue only as you check those boxes. -

And yes, match expenses to revenue when you can—especially if the grant funds specific programs.

Spend first, then release those donor restrictions.

Practical example, because examples rock: If you get a workforce training grant tied to hitting 100 completed

trainings, don’t just claim all the money upfront. Record it as a liability, then recognize revenue one training at

a time when you document completion.

- Read the grant: Is it conditional, restricted, or both?

- Set up liability accounts for conditional pieces.

- Track milestones and eligible expenses in real time.

- Release revenue as you meet conditions and spend on purpose.

Fund Segregation and Tracking

Look, mixing funds is a one-way ticket to audit headaches. Best practice is as clear as a summer day:

- Set up separate funds or subfunds in your accounting system for each grant.

-

Keep a tidy chart of accounts: separate spots for grant revenue, expenses, deferred

income—you name it. - Tag every transaction with a grant ID, program code, and restriction type.

If you can’t pull a report by grant, program, and restriction in under 5 minutes, your tracking needs a tune-up.

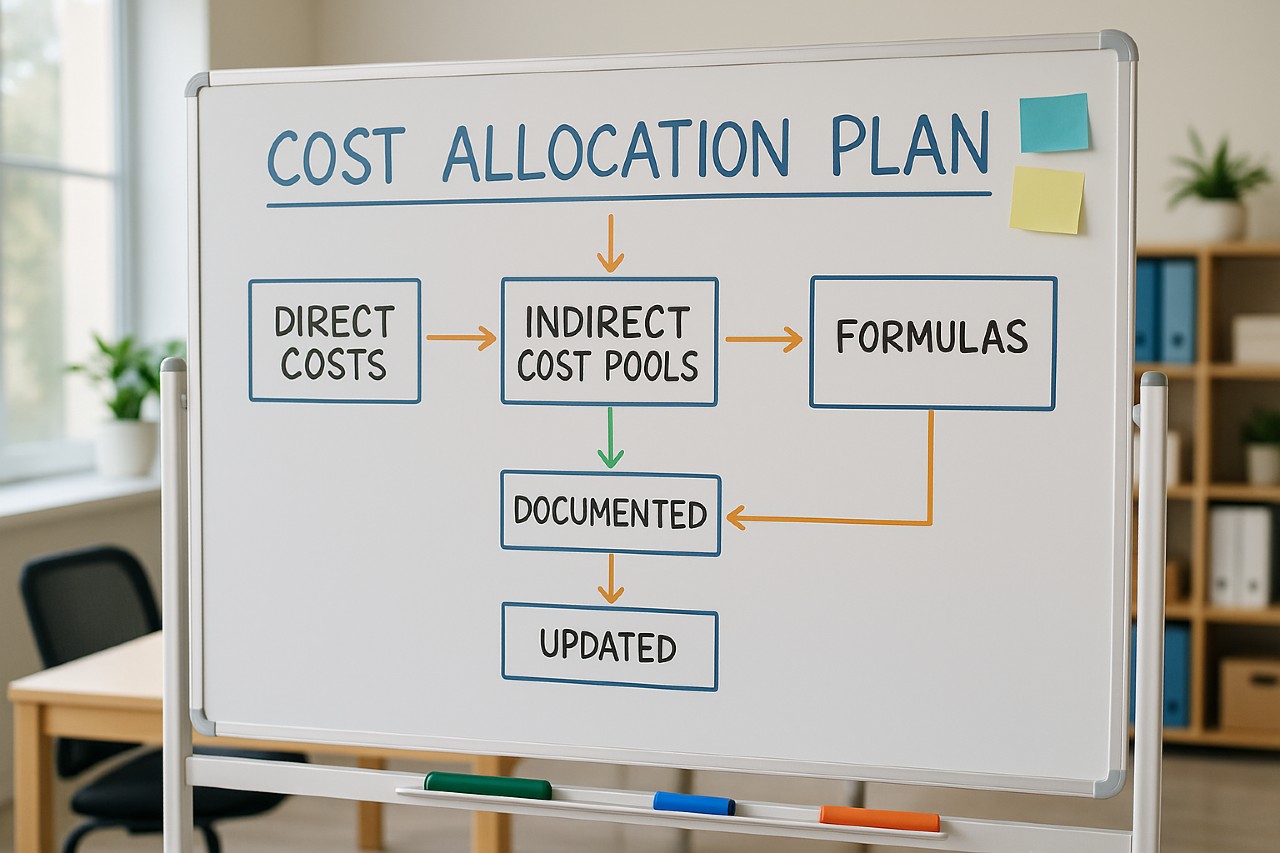

Expense Allocation and Cost Tracking

Not all costs are created equal:

- Direct costs are easy: staff time, materials tied to one grant? Throw ‘em there.

-

Indirect costs (think rent, admin stuff) get tricky—they need a fair allocation method. Maybe it’s

a percentage of labor hours or square footage.

If you’re using a negotiated indirect cost rate or just the 10% de minimis flat rate allowed by federal guidelines,

document that baby like it’s gold. Federal rules require costs to be necessary, reasonable, and allocable (2 CFR Part

200, if you want to get nerdy).

Pro tips:

- Make your grant-funded staff keep timesheets.

- Hold on to grant budgets and watch variances.

- And for the love of audits, document how you allocate indirect costs—and do it the same way every single time.

Think “I can point to the grant that caused this.” Training materials, project staff, travel for that specific program.

Shared expenses like rent, utilities, admin salaries. Allocate using a consistent, documented method—and stick with it.

Accounting for Restricted Grants

What Are Restricted Grants?

Restricted grants aren’t playing around. They come with strings attached—limits on how and when you can use the money.

That might be:

- Purpose restrictions: gotta spend it on a specific program.

- Time restrictions: use it by a certain date (or else).

With ASU 2016-14, nonprofits now report net assets with donor restrictions and those without, which is

way simpler than before.

Recording Restricted Grants

Here’s the gist:

-

For unconditional but restricted grants, recognize revenue right away but stash it under

net assets with donor restrictions. -

Capital grants (equipment purchases, for example), go under revenue when cash hits or conditions are met. Track

fixed-assets separately and spill the beans on restrictions in disclosures.

Releasing Restrictions

When you finally use the money for its intended purpose (or time runs out)—voila! You get to move it from “with

restrictions” to “without restrictions.”

Example journal entry, rolling $10,000 spent on that restricted program:

- Debit: Net Assets with Donor Restrictions — $10,000

- Credit: Net Assets without Donor Restrictions — $10,000

(Yes, accounting can be a soap opera.)

This shuffle doesn’t change your total net assets, just means you kept your promise. Keep all your receipts, invoices,

and program reports ready for show-and-tell with funders or auditors.

- Receive grant → record as revenue with donor restrictions.

- Spend funds on the approved purpose and within the timeframe.

- Release restriction → move amounts to without donor restrictions.

- Disclose the story clearly in your financial statements.

Documentation and Reporting Requirements

- Donor agreements, award letters, proof you did what you said, plus board approvals—keep ‘em all.

- Financial statements need disclosures about restrictions. Transparency is the name of this game.

- And don’t forget funder-specific reports—because each grant loves its own little paperwork party.

Best Practices in Nonprofit Grant Accounting

Implementing Internal Controls and Policies

Listen, internal controls aren’t just buzzwords—they’re your insurance policy against chaos. Top-notch controls include:

- A written grant accounting policy (think clear approval rules and who does what).

- Segregation of duties to avoid a one-person band doing it all.

- Regular bank and grant-to-ledger reconciliations (boring, but oh-so needed).

- Internal reviews of timekeeping, cost allocation, and eligibility documentation.

Single Audits love pointing out weak controls and missing paperwork—so patch those leaks before your auditor shows up with a list.

- ✅ No one person can request, approve, and pay a grant expense.

- ✅ Bank statements and grant reports get reviewed monthly.

- ✅ Timesheets and allocations have backup, not just “trust me.”

Using Grant Management Software

Oh, software—our mixed blessing. It can save you from manual headaches or amplify your chaos if you pick wrong.

Here’s a quick scoop:

- Aplos is gold for small to midsize nonprofits who want tidy fund accounting and donor management without the headache.

- Blackbaud (Financial Edge NXT + Raiser’s Edge) suits mid-to-large orgs needing fancy fundraising + grant reporting mashups.

- QuickBooks Nonprofit fits small budgets but watch out for fund accounting complexity.

- NetSuite Nonprofit Edition is the big league for large orgs chasing robust analytics and grant lifecycle magic.

Look for tools with fund tracking, grant tagging, budgeting, time capture, indirect cost allocation, and audit-friendly exports. Your life will thank you later.

| Tool | Best for | Notes |

|---|---|---|

| Aplos | Small–midsize nonprofits | Clean fund accounting, donor-friendly. |

| Blackbaud FE NXT + RE | Mid–large orgs | Deeper fundraising + reporting. |

| QuickBooks Nonprofit | Budget-conscious small orgs | Make sure fund setup is rock solid. |

| NetSuite Nonprofit Edition | Growing / large orgs | Strong analytics and grant lifecycle tools. |

Staff Training and Communication

If your program folks don’t get grant rules, things go sideways fast. Train them on budgets and what’s allowed.

Finance and programs? They need regular face-time to keep expenses and program progress in synch.

And please, make simple, easy-to-follow guides on how to code costs and file paperwork.

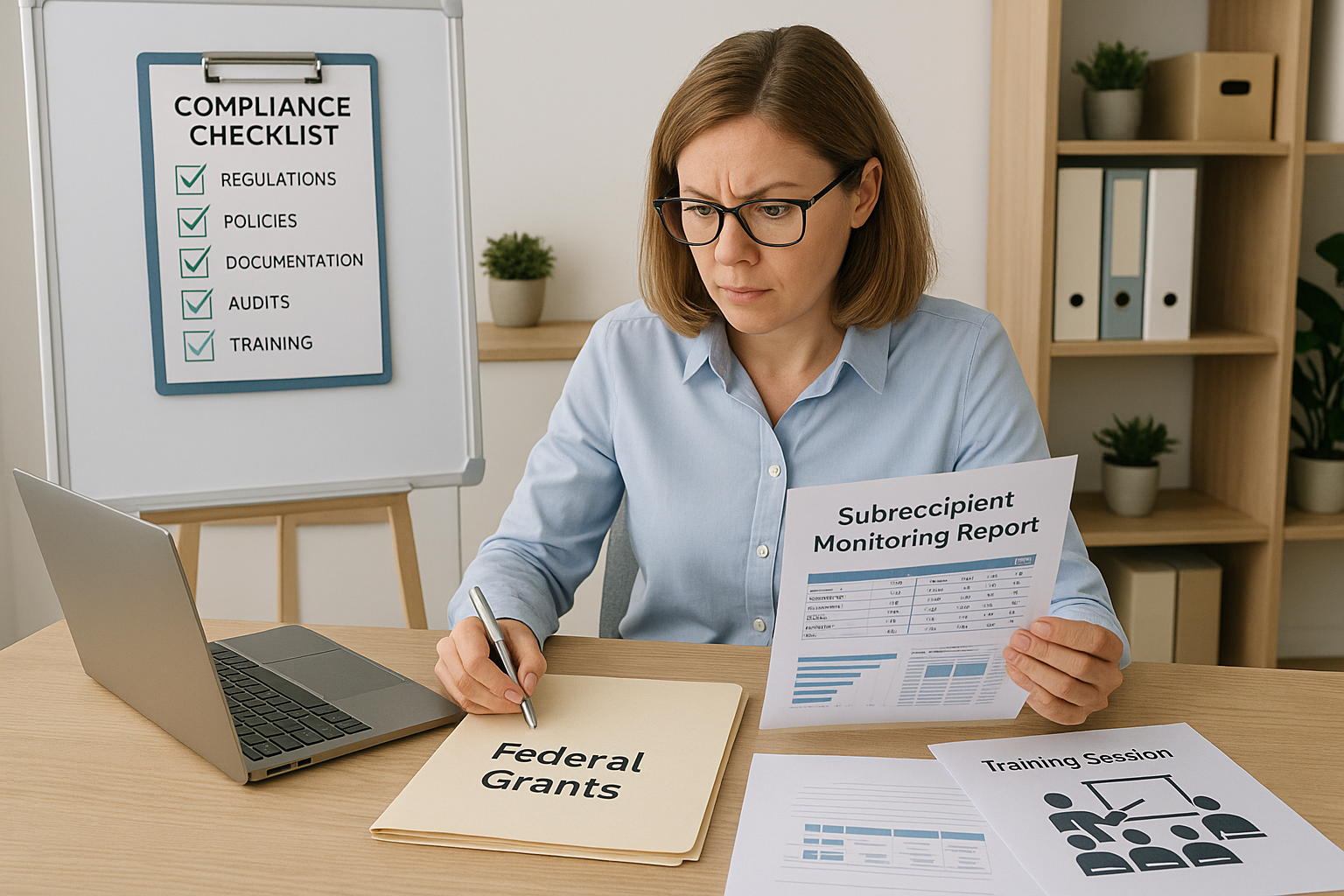

Preparing for Audits and Compliance Reviews

Get a “grab-and-go” grant folder with all award docs, budgets, invoices, payroll, and reports.

Do some pre-audit homework: check that every cost is legit, has backup, and everything ties out.

Auditors tend to sniff out missing docs, misallocated expenses, and sloppy subrecipient monitoring—so catch those gremlins first.

Handling Federal Grants and Compliance the Right Way

Federal grants are the proverbial shiny “audit magnets.” Treat them that way.

Understanding Federal Grant Requirements

Listen, federal rules (Uniform Guidance 2 CFR Part 200) can feel like a riddle wrapped in spaghetti—but here’s what matters:

- Allowable costs must be necessary, reasonable, allocable, and well-documented.

- Some stuff, like entertainment and some fundraising costs, just ain’t allowed.

- Procurement rules, record-keeping, and reporting are strict and timely—no slacking.

For more detail, nerds can check 2 CFR Part 200.

Segregating and Tracking Federal vs Non-Federal Funds

Keep federal award dollars in their own lane—different accounts or GL codes.

Watch those draws vs expenses like a hawk. Federal watchdogs hate it when you hold onto cash without using it or draw down funds without receipts.

Reconcile monthly or quarterly before closeout. Because closeout is no joke.

Monitoring, Reporting, and Communication

Get those financial and program reports in on time—no excuses.

Keep backup docs for every penny reported. Documentation is your superhero cape.

Do internal checks regularly. Catch problems before external auditors do.

Staff Training and Policy Updates for Federal Grants

Update those grant policies with all federal deets.

Train program managers on what costs pass muster and expect to back them up.

Refresh training yearly because rules love to change.

Managing Subrecipient Monitoring and Risk

Passing federal funds to subrecipients? Buckle up, because you’re in charge of oversight (2 CFR 200.331).

That means:

- Risk assessments for each subrecipient.

- Watching their performance and financial reports.

- Collecting their Single Audit info if their spend hits the threshold.

- Keeping a monitoring plan and action steps on file.

You want all your ducks in a row.

Practical Federal-Grant Compliance Checklist (quick)

- Document award terms and budgets.

- Set up grant charts of accounts and funds.

- Use payroll/timekeeping with grant codes.

- Approve expenses against budgets, with a two-step review.

- Reconcile draws to expenses monthly.

- Keep programmatic proof like participant lists and outputs.

- Run risk assessments and schedule monitoring visits.

- ✓ Chart of accounts set up by grant and CFDA number (if applicable).

- ✓ Timekeeping and payroll tie back to grant codes.

- ✓ Drawdowns = documented, eligible costs (no guessing allowed).

- ✓ Subrecipients monitored, with risk levels and follow-ups recorded.

Closing the Loop: Examples and Case Notes

Mini case study (because real talk helps): A midsize nonprofit made the rookie mistake of booking a federal workforce

grant as unrestricted revenue and used it to cover rent. Surprise, surprise—auditors found the misclassification and

“questioned costs” and the organization had to pay back money plus lost future grant chances from that agency. Ouch.

Lesson: Match federal grants correctly to restricted funds and document everything like a U.S. CPA specializing in nonprofits would tell you.

When in doubt, don’t drop federal funds into “unrestricted.” Pause, read the award, and treat it like the restricted,

highly monitored money it almost always is.

Quick software recap:

- Small orgs: Aplos, QuickBooks Nonprofit (but keep those fund controls tight).

- Medium orgs: Blackbaud Financial Edge NXT + Raiser’s Edge.

- Big or growing orgs: NetSuite Nonprofit Edition.

Conclusion — Next steps you can take this week

Grant accounting might not make headlines, but it’s mission-critical. Here’s your quick checklist to go from stressed out to in-control:

- Use a grant-specific chart of accounts and tag every transaction with the grant ID.

- Know if each grant is conditional, restricted, or not, and recognize revenue accordingly.

- Put or tighten internal controls: separate duties, approvals, and pre-audit sweeps.

- Pick a fund/grant-aware software tool that fits your size and budget.

- If you pass funds through, prep a subrecipient monitoring checklist and do a risk assessment for each.

- Train your program folks on what costs are allowed and keep all your docs in one central spot.

Here’s the one thing worth your coffee break right now: whip up a spreadsheet or report listing every active

grant—federal or private, conditional or not—with GL codes, budgets, and next deadlines. That single tool will turn

your board reports from confusing mumble to crystal clear—and save you hours of audit panic.

Want a starter checklist you can grab and customize? Ask your CPA (or shout out to Propel Nonprofits or Aplos for theirs).

Trust me, a clean ledger is your nonprofit’s best friend—keeping your funding and mission safe.

Still reading? You’re my favorite. Now go rock that grant accounting!