Ever stared at your nonprofit’s budget and wondered, “Wait, what giant monster devoured half the admin budget and left crumbs over by Program A?”

Nope, you’re not alone. Functional expense allocation feels like trying to figure out who brought the mystery casserole to the staff potluck—awkward,

a little messy, but absolutely necessary. Do it right, and your board and donors will throw a parade. Screw it up, and you’ll awkwardly explain why

your tutoring grant covered half the coffee stash.

Alright, buckle up. This guide is your friendly sidekick through the wild world of functional expenses. We’ll get into what they are, why people like

donors (and the IRS) lose sleep over them, how to pick allocation methods that don’t make you want to scream, and how to document everything so your

auditors don’t twitch. We’re talking three big functional categories, hands-on cost-allocation tips (with real-deal examples), how it all lands on your

Statement of Functional Expenses and Form 990, plus a cost allocation plan outline you can swipe tonight (or bookmark for later when you have a minute).

Get cozy with these fancy terms: Statement of Functional Expenses, program services expense, cost allocation,

financial transparency, IRS Form 990, and nonprofit accounting. Let’s take that overhead monster by the horns

and turn your functional expense data into a secret weapon—not just for ticking compliance boxes, but for impressing donors and sharpening your game plan.

What Are Functional Expenses in a Nonprofit?

Functional vs. Natural Expense Classification

Picture expenses like ingredients and recipes. Natural classification is the “what you bought” — salaries, rent, supplies, all the dull but necessary stuff

on your grocery list. Functional classification is the “why you bought it” — was it for program services, management and general, or fundraising? It’s like

separating your Kroger haul into “dinner,” “cleaning supplies,” and “wine for morale.”

Under U.S. GAAP (that’s FASB ASC 958 if you wanna get technical) and nonprofit reporting rules, you gotta show both what you spent money on and why. Think of

it as telling your story twice—once by the ingredients and again by the recipe steps (FASB ASC 958; Nonprofit Accounting Basics). It makes things clearer for

anyone snooping through your finances.

The Three Primary Functional Categories

-

Program Services: This is the core stuff that moves the mission needle—program staff paychecks, supplies for the actual work, client travel,

outside help you pay to get the mission done. So, if you’re tutoring, the tutors’ pay and lesson materials? Program services, hands down. -

Management and General (Administration): These are your sidekicks, the folks and costs keeping the whole nonprofit ship afloat. Executive

leadership, bookkeeping, HR, legal fees, board expenses—all those behind-the-scenes essentials that don’t belong to one program but keep the lights on and

governance tight. -

Fundraising: The money-raisers, donor charmers, event planners. Salaries for fundraising folks, campaign flyers, your donor database

software—all the jazz that keeps the cash flowing.

Look, categorizing is like sorting laundry—you want your whites here, colors there. One salary might get sliced and diced across categories if someone’s juggling

program work and fundraising. Consistency’s the key.

Key takeaway: Natural = what you bought. Functional = why you bought it. You need both views to tell a complete, credible financial story.

Why Proper Functional Expense Allocation Matters for Your Nonprofit

Impact on Donor Confidence and Funding

Let’s be real—donors, foundations, and watchdog groups obsess over how much money actually hits the mission. They want to see at least 65–75% (sometimes more,

depending on what you do) going right into program services. Charity Navigator and CharityWatch wave these ratios around like gold stars (Charity Navigator;

CharityWatch). Nail down a crystal-clear, consistent breakdown, and you boost trust, smooth the way for grants, and make big donors smile.

Compliance with Accounting Standards and Form 990

-

FASB wants your expenses shown by both function and natural classification, plus a little “here’s how we split costs” note tucked somewhere in the financial

disclosures (FASB ASC 958). -

Then there’s the IRS Form 990, particularly Part IX, aka the Statement of Functional Expenses playground for bigger nonprofits (Form 990 instructions). If

you’re rolling with gross receipts over certain levels, you gotta spill these details publicly too. Keeping your numbers aligned ensures your filings don’t

cause eyebrow-raises or uncomfortable calls.

If your audited statements and Form 990 don’t play nice, or if your cost allocation game is vague, you’re inviting auditors, grant reviewers, or donor snoops to

knock on your door with questions. Spoiler: that’s no fun.

Operational and Strategic Benefits

Here’s the thing—functional expense data isn’t just an IRS snack. Internally, it’s pure gold.

- It helps you budget better by showing the real price tag of each program (hello pricing and sustainability insights).

- It flags where you might be running on empty. If admin costs look low because staff are working overtime, the numbers will tell you to stop burning candles at both ends.

- It fine-tunes grant budgets and talks for indirect cost recovery. Because, yes, that’s a real thing people talk about.

So yeah, allocation isn’t just about playing nice on paper. It helps you run your nonprofit smarter, not just squeaky clean.

Pro tip: Track and share your program vs. admin vs. fundraising ratios in board packets and donor decks—don’t wait for people to dig through your 990 to find them.

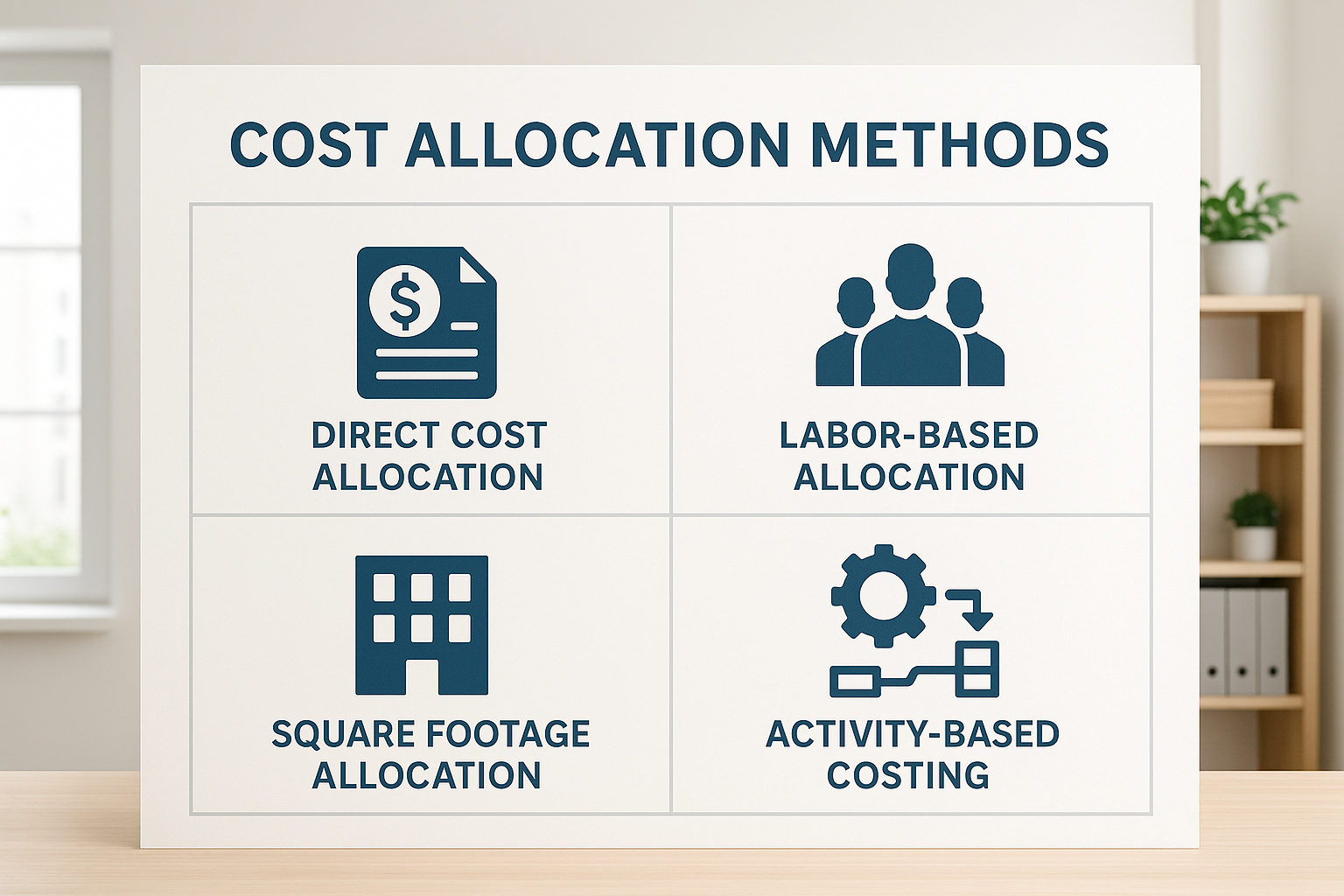

Cost Allocation Methods for Nonprofits Explained

Direct Cost Allocation

If you can point to a cost and say, “That belongs right over here,” do it. Someone working solely on Program A? Put their salary in program costs and call it a

day. This direct identification method is the easiest to defend and least likely to cause headaches (FASB ASC 958).

Indirect Cost Allocation Methods

When stuff benefits more than one function, pick a fair way to divvy it up based on a cost driver. Some favorite ways:

| Method | When It Works Best |

|---|---|

| Labor-Based (FTE or Salary %) |

Works well when expenses follow people around, like HR or office supplies. For example, if program staff make up 70% of employees, allocate 70% of HR costs to programs. |

| Square Footage | Perfect for stuff like rent and utilities. If programs occupy 6,000 sq ft of a 10,000 sq ft space, they get 60% of the rent. Simple and solid. |

| Participant-Based Allocation | When costs relate to how many clients you serve (think training materials per person). |

| Activity-Based Costing (ABC) |

Fancy and detailed. Assign costs by specific activities then to programs. Great if your nonprofit’s a big beast with complex ops, but it’s a data muncher. |

| Step-Down (Sequential) Method | Allocate support services step-by-step. IT and Facilities get allocated first, then admin costs. It’s like peeling an onion, but for costs. |

| Percentage of Direct Costs | Overhead gets divvied up based on each program’s share of direct costs. Easy but not the sharpest tool if your staff or space usage is all over the map. |

Hot take incoming—labor-based and square footage are your everyday workhorses: easy, defensible, and everyone’s cool with them. Activity-based or step-down give

precision but need more brainpower and data intake.

Selecting the Right Method for Your Organization

Here’s what to think about:

- Size and complexity. Smaller nonprofits often stick with FTE or salary slices; the big players can go full ABC or step-down fancy.

- Funder rules. Some federal grants don’t play nice with just any allocation plan.

- Data availability. Don’t pick a method you can’t actually figure out.

- Reasonableness. Your choice has to reflect reality, and be easy to explain when auditors or funders come knocking.

Your next step: Circle 1–2 methods you can actually support with data today, and commit to using them consistently for at least a year.

Developing and Documenting a Cost Allocation Plan

Components of a Cost Allocation Plan

A solid plan lays it all out:

- Why you’re doing this and what’s included

- Clear definitions of functional categories

- How you identify direct costs

- What pools of indirect costs exist and how you split ’em (the formulas, please)

- Where your data comes from and how often you crunch the numbers

- Who’s responsible for running the show and signing off

- How and when you update the plan, plus board oversight

Sample outline to steal:

- Introduction and policy vibe

- Functional categories explained

- Direct cost rules

- Indirect cost pools and allocation rules (with formulas!)

- Examples with sample numbers anyone can get

- What records to keep and for how long

- How often you check and approve the plan

Best Practices for Consistency and Compliance

- Document everything. Auditors love clear disclosure—they want to know your secret sauce.

- Update this annually or whenever your nonprofit does a big shuffle.

- Train your people and board. Everyone needs to get why this matters.

- Keep the methods simple and repeatable. Being defensible beats being clever every time.

- Run practice rounds. Check how your allocations shake out on budgets and reports.

Common Challenges and How to Overcome Them

- Shared staff split between roles? Use time studies, timesheets, or carefully documented estimates, approved by the boss.

- Space usage that wiggles month to month? Average it over the year.

- Grant restrictions making your life complicated? Keep those funds separate and make sure costs charged to grants match rules; allocate indirects as the grant says.

- Staff grumbling about allocations? They don’t steal program money—they just show the true cost so you can ask for more funds honestly.

Practical tip: don’t be fancy right away. Start with simple labor or square-footage allocation and graduate to activity-based costing once you have the bandwidth.

Quick recap: Put your rules in writing, keep them simple, and update them when your org structure or funding shifts in a big way.

The Statement of Functional Expenses and Form 990 Reporting

What is the Statement of Functional Expenses?

Think of the Statement of Functional Expenses as the “show me the money” chart. It spells out your expenses by both function and nature. You might see it as

its own statement, part of your Statement of Activities, or hidden in the notes. This statement keeps you transparent and is what auditors expect to see front

and center (FASB ASC 958; AICPA guidance).

Functional Expenses Reporting on IRS Form 990

- Form 990’s Part IX is the spot where functional expenses go public. It lists line items like salaries, rent, fees, and expects you to split ’em between programs, admin, and fundraising (IRS Form 990 instructions).

- If you file 990-EZ or 990-PF, your reporting is lighter. But if you do the big Form 990, Part IX is your jam.

- And don’t let totals get out of sync—Part IX, Part I of Form 990, and your audited statements should all sing the same tune.

Tips to Ensure Accuracy and Compliance in Reporting

- Cross-check, cross-check, cross-check. Make sure Part IX matches your ledger and audit papers.

- Use the same allocation methods year after year and spill the beans about any changes in your notes.

- Software is your friend here. Blackbaud, QuickBooks for Nonprofits, Aplos—these can help map expenses and keep track.

- Save your backup stuff: timesheets, space measurements, allocation worksheets. Audit time is not the time to scramble.

- If someone questions your numbers, don’t improvise. Show them your documented methods and calculations. Confidence, people!

Key takeaway: Your Statement of Functional Expenses and Form 990 should tell the exact same story as your internal books—no plot twists.

Sample Cost Allocation Example (Quick Walkthrough)

Imagine this:

- Total rent is $120,000 a year

- Office size: 10,000 sq ft

- Programs get 6,000 sq ft, Admin 2,000 sq ft, Fundraising 2,000 sq ft

The math:

- Program gets 6,000/10,000 = 60%, so $72,000 of rent

- Admin gets 20%, $24,000

- Fundraising also 20%, $24,000

Now, HR costs come in at $60,000, allocated by FTE:

- Program staff: 12

- Admin: 3

- Fundraising: 2

- Total: 17

So:

- Program HR = 12/17 = about 70.6%, $42,360

- Admin HR = 3/17 = 17.6%, $10,560

- Fundraising HR = 2/17 = 11.8%, $7,080

You’d roll these numbers into your Statement of Functional Expenses under rent and employee benefits, with formulas documented so nobody questions the math.

Pro tip: Build a simple spreadsheet tab for each major cost pool (rent, HR, IT) with the exact formulas you’ll reuse every year.

Conclusion — Key Takeaways and Next Steps

– Functional expense allocation isn’t just tax paperwork—it matters to donors, funders, regulators, and your own strategy. It’s a tool, not a chore.

– Pick allocation methods that make sense, hold up under scrutiny, and you can live with year after year. Labor-based stuff and square footage get most of the job done; step-down and activity-based add precision if you’re bigger and hungrier for details.

– Get a written cost allocation plan down (using the sample outline above), update it every year, and make sure your team understands what’s up.

– Your Statement of Functional Expenses, Form 990 Part IX, and audited statements should all tell the same story—no plot holes, no confusion. That’s how you keep regulators and donors happy (IRS Form 990 instructions; FASB ASC 958).

Okay, here’s a real-world nugget from a U.S. CPA who spends all day helping nonprofits like yours (shout-out to the Telos CPAs crew). Take a peek at your

allocation plan this quarter. If you don’t have one, draft a quick one-page version slapping together a policy and try running rent and HR cost allocations

for last year. Watch your program ratios wiggle. When you get stuck, call a pro—getting it right early saves you endless awkward donor calls and board

explanations.

Good governance plus clear allocations means stronger donor trust and smarter decisions. Time to show your board the real cost of making a difference. And

hey—hide those potluck crumbs before next time!

Still reading? You’re my favorite.

Your next step: Block 60 minutes this week to sketch your cost allocation plan, test it on last year’s rent and HR, and note any questions to bring to your CPA.